TL;DR — Executive Snapshot President Prabowo Subianto's announcement at the Japan-Indonesia Forum in Tokyo on 31 March 2026 set an ambitious target of 100 gigawatts (GW) of solar power capacity within three years, deployed primarily through a nationwide rural and village-level deployment programme (The Jakarta Post, 2026). With Indonesia's current domestic solar manufacturing capacity standing at only around 5 GW per year and an estimated financing gap of USD 78 billion to close by 2030 (IESR, 2026), the target creates a generational opportunity for domestic manufacturers, infrastructure developers, and component suppliers. PT Apollo Solar Indonesia stands as a homegrown contributor to this national agenda — proudly built in Batam, TKDN compliant, and Made in Indonesia — operating a 500 MW per year production facility and serving as a member of APAMSI (Asosiasi Pabrikan Modul Surya Indonesia). The path to 100 GW will be built by domestic manufacturers committed to Indonesia's energy future, and Apollo Solar Indonesia is proud to be part of that journey.

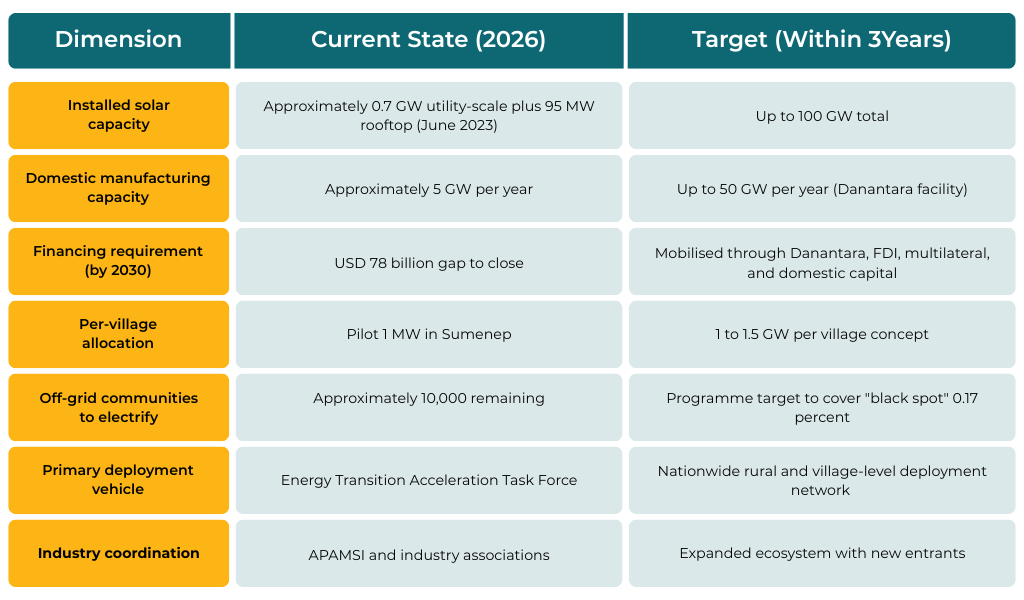

Indonesia is at the threshold of one of the largest decentralised solar deployments ever attempted in the world. President Prabowo Subianto's 100 GW target, announced multiple times across high-profile forums in 2025 and 2026, has moved from political ambition to operational mobilisation. The Energy Transition Acceleration Task Force, chaired by Indonesia's Minister of Energy and Mineral Resources (ESDM), Bahlil Lahadalia, has been established. State asset manager Danantara has been positioned as the primary investment vehicle. A 1 MW pilot project in Sumenep, East Java, has been completed as a technical reference model.

What this means for the national solar industry is no longer theoretical. Domestic manufacturers, EPC contractors, balance-of-system suppliers, and component producers face a market demand multiplier rarely seen in any industry over such a short horizon. Yet the same demand creates structural challenges: financing gaps, manufacturing capacity constraints, regulatory consistency questions, and the need for bankable projects at scale. This article examines what the 100 GW target means in practice, how the opportunity is distributed across the value chain, what challenges remain, and how domestic players including Apollo Solar Indonesia fit into the broader national agenda.

What Is Indonesia's 100 GW Solar Target and Why Is It Significant?

Indonesia's 100 GW solar target is a national programme announced by President Prabowo Subianto to build 100 gigawatts of solar power capacity within three years, deployed primarily through a decentralised cooperative-based deployment network across villages and regions. The target represents one of the largest decentralised solar deployments ever planned globally and aims to strengthen energy self-sufficiency, expand rural electricity access, and reduce fossil fuel imports.

The strategic significance operates across three dimensions:

- Energy security. Indonesia continues to rely heavily on imported fossil fuels, exposing the economy to global price volatility. Domestic solar reduces this exposure structurally, not cyclically.

- Rural electrification and energy equity. Although Indonesia's electrification ratio has reached 99.83 percent, approximately 10,000 remote communities remain off-grid, representing the final 0.17 percent of "black spot" areas that the programme aims to address (Indonesia Business Post, 2026).

- Economic transformation. The programme is positioned not solely as an emission target but as expanding energy access, reducing costly fuel imports, and shielding the domestic economy from global energy price volatility, according to officials from the Energy Transition Acceleration Task Force.

The 100 GW figure also positions Indonesia among the most ambitious solar deployment programmes in Asia Pacific, comparable to large-scale national initiatives in China, India, and Vietnam during their solar acceleration phases.

How Big Is the Current Manufacturing Gap and What Does It Mean for Domestic Players?

The current domestic manufacturing gap is substantial. Indonesia's existing solar module manufacturing capacity stands at approximately 5 GW per year, while the 100 GW target over three years implies a theoretical demand of around 33 GW per year, leaving a structural gap that must be filled through a combination of domestic capacity expansion, foreign investment partnerships, and module imports during the initial ramp-up phase.

Energy Minister Bahlil Lahadalia has been explicit about this gap, stating that domestic industries can currently produce no more than 5 GW per year, making outside investment critical (Jakarta Globe, 2025). The government's response has been multi-pronged:

- Foreign investor mobilisation. Indonesia has actively courted foreign investors, particularly from Japan during the Indonesia-Japan Business Forum, to bring capital and technology partnerships.

- Major domestic manufacturing investment. Investment Minister Rosan Roeslani, who also heads BPI Danantara, announced a USD 1.4 billion investment in a new domestic solar manufacturing facility expected to produce up to 50 GW of solar panels annually, far exceeding previous estimates of Indonesia's photovoltaic manufacturing capacity (Indonesia Business Post, 2026).

- Industrial repurposing. The Cirebon-1 coal-fired power plant, planned for early retirement, is estimated to attract investment worth USD 198 million for the construction of a solar panel and electric battery factory (Indonesia Business Post, 2025).

For existing domestic manufacturers such as Apollo Solar Indonesia, which operates a 500 MW per year production facility in Batam, this environment creates both opportunity and competitive pressure. The opportunity is clear: domestic demand for solar modules will dwarf current supply for the foreseeable future. The pressure is also clear: new entrants with massive capacity will compete for the same demand, making product differentiation, certification, and TKDN (Tingkat Komponen Dalam Negeri) compliance increasingly important.

What Are the Investment and Financing Dynamics Behind This Target?

The investment and financing dynamics behind the 100 GW target are characterised by a significant gap that must be closed through multiple capital sources. IESR estimates a financing requirement of USD 78 billion to close by 2030 to achieve the target, covering photovoltaic farms, storage systems, transmission infrastructure, and domestic manufacturing capacity expansion (IESR, 2026).

The financing architecture taking shape involves four primary channels:

Government-backed investment vehicles. BPI Danantara has emerged as the main investment and financing vehicle tasked with mobilising capital for rollout. Its role is to coordinate state-backed resources, including potential cross-subsidies from existing energy sectors and strategic asset partnerships.

Foreign direct investment. Japan, China, Korea, and Middle Eastern sovereign wealth funds have been identified as potential financing partners. The Japan-Indonesia Forum in Tokyo on 31 March 2026 was specifically used as a platform to engage Japanese business leaders.

Multilateral development finance. Institutions such as the Asian Development Bank and the World Bank are expected to play roles in concessional financing for rural electrification components of the programme.

Domestic capital markets. Bond issuance, green sukuk, and project finance structures channelled through domestic banks form the fourth pillar, particularly for bankable utility-scale projects.

The investment opportunity is not limited to large-scale capital deployment. Component manufacturing, balance-of-system supply, EPC services, operations and maintenance, and value-added technology integration represent layers of the value chain that domestic small and medium enterprises can participate in.

What Role Will Domestic Manufacturers Like Apollo Solar Indonesia Play?

Domestic solar manufacturers play a critical role in achieving the 100 GW target through three interconnected dimensions that define why local manufacturing matters: strengthening Indonesia's energy independence, driving tangible economic value across the national economy, and supporting sustainable growth through shorter logistics chains and lower emissions. Beyond cost considerations, domestic production represents economic sovereignty and quality assurance for projects under the national agenda.

Pillar 1: Strengthening Energy Independence

Local production directly reduces Indonesia's reliance on imported solar modules, mitigating exposure to global supply chain disruptions, geopolitical tensions, and trade policy shifts. For a programme of 100 GW scale, dependency on external suppliers represents a systemic risk that domestic manufacturing capacity addresses structurally. Modules manufactured within Indonesia ensure continuity of supply for projects critical to national energy infrastructure, particularly under village-level and rural deployment programmes that require nationwide rollout.

Pillar 2: Driving Economic Value

Domestic solar manufacturing creates a multiplier effect across the national economy: local employment in production facilities, talent development in solar engineering and quality control, supplier ecosystem growth for raw materials and components, and tax contributions that flow back into national development. Each gigawatt of locally produced capacity translates into industrial jobs, skills transfer, and value retention within Indonesia rather than flowing out as import costs. For the 100 GW programme, domestic manufacturing is the channel through which the energy transition also becomes economic transformation.

Pillar 3: Supporting Sustainable Growth

Local production reduces logistics emissions associated with importing modules across long distances, contributing to a lower carbon footprint of the solar deployment itself. Shorter logistics chains also mean faster project delivery, easier warranty handling, and reduced infrastructure stress on Indonesia's ports and inter-island shipping. The sustainability case for domestic manufacturing extends beyond clean energy generation to encompass the lifecycle footprint of how that capacity is built and maintained.

Apollo Solar Indonesia's Profile and Product Lineup

Apollo Solar Indonesia exemplifies the profile of a domestic manufacturer positioned to contribute to this national strategy. As a PMDN (Penanaman Modal Dalam Negeri) company with a 500 MW per year production facility completed in Batam in February 2023, Apollo operates within Indonesia's industrial fabric rather than as a foreign subsidiary. As a member of APAMSI (Asosiasi Pabrikan Modul Surya Indonesia), Apollo participates in industry coordination on technical standards, policy advocacy, and market development. The company's status as Made in Indonesia and TKDN compliant aligns with the procurement priorities of government-backed projects under the 100 GW agenda.

Apollo's product lineup is engineered for Indonesian conditions and use cases across the value chain:

- Bali Series. 10BB HALF-CELL design with N-Type TOPCon Bifacial Double Glass, efficiency up to 22.44 percent, power output 555W to 580W. Suitable for premium residential and commercial installations.

- Java Series. 16BB HALF-CELL N-Type TOPCon, efficiency up to 22.54 percent, power output 415W to 630W. The widest power range in the lineup, suitable from compact residential to large commercial.

- Kalimantan Series. 12BB HALF-CELL Monocrystalline PERC, efficiency up to 21.57 percent, power output 535W to 670W. Engineered for the broadest installation footprint including industrial-scale projects.

- Sumatra Series. 10BB HALF-CELL Monocrystalline PERC, efficiency up to 21.48 percent, power output 530W to 555W. A reliable entry choice for households and small businesses.

- APMR-UPLDD 132 Series (Tier-1 Flagship). HALF-CELL N-Type Bifacial Double Glass Monocrystalline with 24.06 percent maximum efficiency, power output 620W to 650W, certified as a Global Tier 1 bankable brand with 30 years output guarantee. This flagship positions Apollo at the upper tier of global module performance for utility-scale projects requiring bankable international credentials.

This product breadth allows domestic manufacturers like Apollo to serve multiple deployment scenarios within the 100 GW programme, from village mini-grids (small to medium installations) to utility-scale projects (high power output modules) and rooftop deployments (premium efficiency series).

What Challenges Must Be Navigated to Achieve the Target?

The 100 GW target faces several practical challenges that the government, industry, and investors must navigate together, including financing gaps, slow phase-out of existing diesel power plants, the need for bankable Power Purchase Agreements (PPAs), regulatory consistency between ad-hoc programmes and the existing electricity plan (RUPTL), and the speed of domestic manufacturing capacity expansion to avoid over-reliance on imports.

The most material challenges include:

Financing mobilisation speed. The USD 78 billion financing gap is not just a number but a pacing constraint. Capital must be mobilised at a rate that matches manufacturing and project deployment, or the entire programme risks stalling at critical milestones.

Bankable project pipelines. Indonesia's renewable energy track record has been hampered by a slow phase-out of existing diesel power plants and a lack of signed PPAs despite enabling regulations passed in 2022 (PVKnowhow, 2026). Without bankable projects, even abundant capital cannot deploy efficiently.

Manufacturing capacity ramp-up. Even with the USD 1.4 billion Danantara investment targeting 50 GW per year of manufacturing capacity, the timeline to operationalise that capacity is measured in years, not months. The gap between announced plans and operating capacity creates a transition period dependent on imports.

Regulatory and policy consistency. Critics have raised concerns that launching such a large-scale project outside the RUPTL risks undermining the national electricity plan, potentially complicating investment decisions for developers and increasing uncertainty about prioritisation of future infrastructure projects (Windonesia, 2026).

Workforce and skills development. Operating 100 GW of solar capacity requires not only modules and installation but also long-term operations and maintenance workforce. Skills development in solar engineering, inverter maintenance, and grid integration must scale in parallel.

These challenges are not arguments against the target. They are coordinates for serious investors, manufacturers, and decision-makers to map their participation strategy.

Snapshot of the National Solar Opportunity

The table below summarises the scale and structure of Indonesia's 100 GW solar opportunity:

How Apollo Solar Indonesia Contributes to the National Solar Agenda

At Apollo Solar Indonesia, we are proud to be part of Indonesia's journey to 100 GW. As a PMDN (Penanaman Modal Dalam Negeri) company with a 500 MW per year production facility in Batam, we contribute to the national agenda through certified domestic manufacturing capacity, a product portfolio engineered across residential, commercial, and industrial use cases, active participation in APAMSI for industry coordination, and operational alignment with TKDN compliance for government-procured projects. Proudly homegrown. Built in Batam. Made for Indonesia.

For developers, EPC contractors, and procurement decision-makers evaluating solar module sourcing for projects under the national 100 GW programme, domestic manufacturers offer practical advantages: shorter delivery lead times, easier warranty claims handling, support for TKDN compliance in government-procured projects, and contribution to the broader development of Indonesia's renewable energy ecosystem. The choice between domestic and imported modules is not just a cost calculation but also a strategic alignment with national industrial policy.

We welcome engagement with developers, government planners, and industry stakeholders working on projects aligned with the national 100 GW agenda. Whether for utility-scale projects, commercial rooftop deployment, or rural electrification, Indonesia's domestic solar industry has the technical capacity and engineering expertise to participate meaningfully. The path to 100 GW will be built one project at a time, and we stand ready to participate alongside national and international partners in achieving this generational target.

Proudly part of Indonesia's journey to 100 GW. Brighten the Future with Apollo Solar Indonesia.

For developers, EPC contractors, and decision-makers exploring solar module sourcing for projects aligned with Indonesia's national solar agenda, the Apollo Solar Indonesia team is open to discussions on technical specifications, production capacity, and project-fit assessments.

Sources

- The Jakarta Post. (2026). "Prabowo Pledges 100 GW Solar Energy Target Within Three Years." Published 31 March 2026.

- Indonesia Business Post. (2026). "Prabowo's 100 GW Solar Plan Puts Villages at the Center of Indonesia's Energy Transition."

- Indonesia Business Post. (2025). "Prabowo Pushes for Village Solar Plants, Eyes 100 GW National Capacity." Published 16 September 2025.

- Jakarta Globe. (2026). "Prabowo Targets 100 GW Solar Power Buildout in Two Years." Published 13 March 2026.

- Jakarta Globe. (2025). "Indonesia Eyes Foreign Investors for 100 GW Rural Solar Power Plan."

- PVKnowhow. (2026). "Indonesia Solar Power: Task Force Aims for Stunning 100 GW."

- Institute for Essential Services Reform (IESR). (2026). "Indonesia Needs USD 78 Billion Until 2030 for 100 GW Solar Push."

- Windonesia. (2026). "Indonesia Pushes 100 GW Solar Plan Beyond RUPTL."

- Coordinating Ministry for Economic Affairs of the Republic of Indonesia. (2026). Joint Report with IESR on 100 GW Solar Pathway.

- Apollo Solar Indonesia. (2026). "Product Catalog: Bali, Java, Kalimantan, and Sumatra Series."